Money used to be local. The first non-precious metal coins emerged as a natural consequence of trade, and were seldom accepted as currency outside the city-state on the Grecian coast that minted them. Then nation-states emerged and central banking was invented as an institution. Fiat currencies were deigned into circulation and the connection between money and place was mostly lost. Today, a dollar printed in West Point is the same dollar wherever it is found, whether it’s Dubuque or Dubai. It derives its value from the law of the United States and that law has no physical home. The United States of America, like all other countries, is a polygon on a map, a theoretical construct, a policy document.

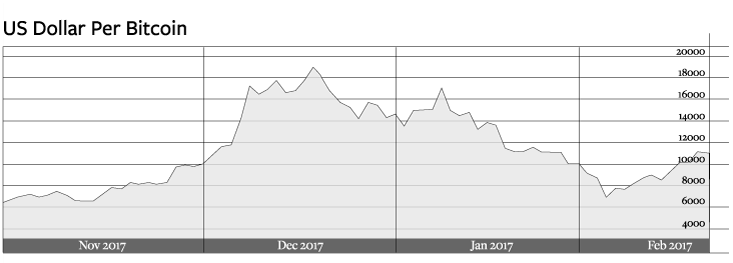

As the dust settles on the haboob that cryptocurrencies have become over the last year or so and we try to find things of lasting value from the wreckage, we should keep in mind this missing piece of the puzzle: All resilient things start local. To find inherent value and stability digital currencies need to ground themselves somewhere. They need to go local. A theoretical construct is no longer enough. Digital currencies need something more tangible than just value by decree. They need a physical place where people can go and where the token will always be valued and the debts will always be paid. They need a city.

From the city’s perspective it makes perfect sense. Most cities struggle with securing the finances they need. Cities are taut systems operating at the edges of possibility, constantly optimizing the resources that are available to them. Consider New York, one of the richest cities in the world, with an economy larger than Mexico’s. Despite its wealth, it has attracted much negative recent attention for having a drastically underfunded public transport system. Something like $100 billion is needed to fix the New York subway, and nobody knows where that money is going to come from. Almost every city has a laundry list of essential projects that are in dire need of cash. Launching a digital currency for a city could effectively crowdfund these projects.

Only people willing to bet on the city and not just on the currency will make large long-term investments.

Here’s how it would work. New York simply announces that starting on a given day, a digital currency, let’s call it NYCTokens, can be purchased from subway station kiosks. These would be redeemable toward civic services inside the city, like subway rides, health clinics, utility bills, city taxes, hospital or school bills—basically any services that the city provides directly, or for which the city could work out a mutually beneficial arrangement with a third party. The city would also publish an app that would allow anyone to send or receive tokens. However, new tokens would have to be purchased in person at a physical location. The city wouldn’t sell the tokens online or let a third party set up an exchange. By blocking mass-scale transactions in this manner, scalping and mass speculative trading would be discouraged.

The most important question is where NYCTokens derive their value. What will they be “pegged” to and how will the important problem of cryptocurrency volatility be solved?

There’s a very neat two-word answer to all these questions.

Property values.

The value of each NYCToken is pegged to property values. One NYCToken, for example, could be made equal to the market value of 1 square centimeter of New York real estate. At a current costs per square foot of say $1,500, that works out to about $1.60 per token. The city maintains an up-to-date ledger of all property sales, and as the average value of property changes, the value of the NYCToken rises or falls. The number of NYCTokens in circulation corresponds exactly to the total covered area of the city and more tokens will be brought into circulation if and only if the city’s real estate area increases through vertical or horizontal development. Increases in token price represent an increase in real estate value, which can be considered a weak proxy for standard of living, and increases in token number represent city growth.

By buying tokens citizens get the opportunity to invest their surplus income in an asset that is a store of value, an investment with the potential for real appreciation, and a currency that can be used to buy urban services. Instead of adding dollars to her subway card, for example, a city resident could add NYCTokens. The next day, she could spend her tokens to gain entry to the subway system. But if she hangs on to her tokens and they double in value, she could then purchase two subway rides for the same number of tokens. The growing prosperity of the city translates directly into an improved quality of life for its residents, through effectively cheaper urban services.

The prospect of rising token values will attract many citizens to invest in tokens, especially in big cities like New York where property prices are considered a safe bet. The tokens will also attract some investment money from parties who are unlikely to ever trade them for urban services: hedge funds, banks, individual investors, and non-residents. An informal economy will emerge out of people replacing some of their cash transactions with the token transactions on the app. In due time taxing these transactions could also become a source of revenue for the city. In principle, the price of tokens on this informal market may rise above the price supported by the city. But it is unlikely to fall below the price supported by the city, since tokens can always be traded in for real services at the official price.

The net effect of both individual and institutional interest in tokens will combine to produce the same phenomenon: a fresh stream of critical capital for the city to invest in urban development projects. Having their money directly invested in the city will inspire citizens to get more involved in development and political decision making. And since the money raised will be invested back into the city in a way that raises property values (like subway construction projects), tokens would create a self-reinforcing prosperity loop.

There will be complications, of course. A big one will be the legality of a city-based currency. In many countries, cities don’t have the legal authority to issue their own currencies. That, however, is a problem that can be easily solved. Just make sure not to call your new digital object a currency, or money, or coin, or any variants thereof. Make it a subway ride credit. Or school lunch credit, electricity credit, gas credit. Heck cut a deal with Uber and call it Uber credit. The point is that there are many other tokens of value in circulation inside cities that can all stand for “unit of value.”

Digital currencies need a physical place where the token will always be valued and the debts will always be paid.

Another problem to solve would be the volatility brought about by secondary speculative trading. This is naturally tamped by the fact that the token can only be redeemed through urban services. The liquidity of the token for the speculative investor will be naturally limited. Only people willing to bet on the city and not just on the currency will make large long-term investments.

It should be noted that a number of countries, including Saudi Arabia, UAE, Venezuela, and even city-states like Dubai, have already started considering their own cryptocurrencies. But these efforts do not peg their digital currencies to the cost of local services. A cryptocurrency backed entirely by urban fiat has the potential for being the worst of both worlds: It combines an arbitrary, centralized valuation with the potential volatility of cryptocurrencies. Similarly, combining the blockchain with centralized control makes no sense. The solution to currencies dissociated from the value they are supposed to represent is not another floating abstraction made even more volatile by a publicly distributed ledger, but a re-grounding and return to intrinsic value.

Money has traveled around the world in the last 2,000 years and almost freed itself from grounded constructs and borders. Some say this is the root of all evil: Capital is free to move, while individuals are tied up in innumerable layers of bondage from national laws to company policies. In the age of digital we’ve come to believe that new solutions have to be universal, but that need not always be true. In many ways modern interest-based money has been the prodigal son of our civilization. It has fueled exponential growth, but it has also become too abstract a construct to control.

Maybe it’s time for money to come back home.

Fouad Khan has a Ph.D. in urban development science and policy and has worked for the World Bank, UN, and WWF among others in the past. He is currently an associate editor at Springer Nature and tweets at @fouadmkhan.